-

Key Brands

-

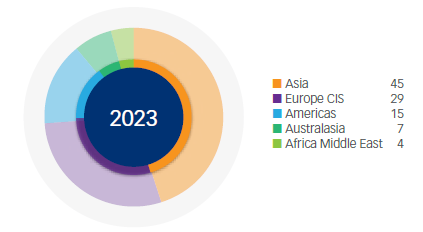

Revenue

-

Performance

-

Prospects

Sterile Focus Brands first half performance was negatively impacted by the COVID lockdowns in China and the ongoing Russia-Ukraine war. However, the second half enjoyed a strong rebound with reported revenue increasing by 14% (CER +2%) compared to H2 2022. This positive turnaround was primarily driven by improved performance in the Americas and the lifting of lockdowns in China resulting in a robust second-half performance relative to the corresponding prior year. Full year revenue grew by 3% (CER -6%) to R10 588 million aided by the strong second half performance and exchange rate tailwinds.

The gross profit percentage of 60,6% was closely aligned with the previous financial year (FY2022: 60,7%) despite inflationary and logistical pressures, external supplier challenges and the negative impact of VBP in China. Continued cost of goods savings from insourcing anaesthetic production and a favourable sales mix have been key contributors.

Revenue and EBITDA performance in FY2024 is anticipated to be adversely impacted by potential VBP risk in China on two products being Fraxiparine and Diprivan. To mitigate this VBP risk, potential acquisitive opportunities are being actively explored to diversify and de-risk the product portfolio in that country on a sustainable long-term basis.

The plan to transfer a large proportion of our anaesthetic portfolio from third-party contractor sites to Aspen-owned facilities in South Africa, France, and Germany has progressed with estimated cumulative savings of R400 million being achieved since inception. Delays in the South African and French facilities, primarily due to the reprioritisation of vaccine production and disruptions caused by COVID in previous years, have been particularly impactful. Consequently, the completion timeline and the extent of cost-saving advantages have extended beyond the initially communicated target of the 2024 financial year. This extension now spans an additional 18 to 24 months with a further R400 million of savings expected over the FY2024, FY2025 and FY2026 financial years.