-

Key Brands

-

Revenue

-

Market Data

-

Performance

-

Prospects

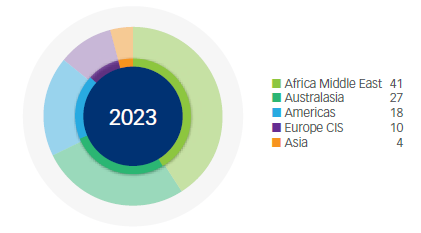

Growth momentum has been achieved in all regions. Africa Middle East, which is the largest region, grew 3% (CER +1%) on a comparable basis when excluding the prior year product portfolio divestment in South Africa (R381 million). Australasia, the second largest region, grew 15% (CER +7%) underpinned by strong growth in its OTC portfolio of 21%. Regional Brands have demonstrated resilience, stability, and consistent growth in an environment marked by global volatility.

The gross profit margin saw a notable increase, rising from 56,5% in the previous year to 59,6%. This improvement can be attributed to a favourable sales mix and cost of goods savings, which effectively counteracted inflationary headwinds.

Based upon current exchange rates, double digit revenue growth is expected with a heavier H2 2024 weighting supported by base business organic growth and the recently announced product portfolio additions in Latin America and South Africa.

The South African business has a respected, professional and capable footprint across Southern Africa which has provided the foundation to attract further multinational partnerships providing mutual benefits by significantly outperforming a small standalone local entity. For Aspen, these collaborations provide it with access to new chemical entities (“NCEs”), biosimilars, branded products and a research-based pipeline without commoditisation risks. The annualised sales from the deals announced with Lilly and Amgen will be more than R800 million and over the medium term will be significantly enhanced by pipeline molecules inter alia including the following:

- From Lilly, which has one of the strongest pipelines globally, the anticipated registration and launch of Mounjaro in CY2024 plus five other NCEs to be launched in the short term covering oncology, immunology, pain and diabetes

- Biosimilar and NCE launches from Amgen in the short term in the therapeutic areas of oncology, immunology and ophthalmology complemented by a strong medium-term pipeline.

In Latin America, the recently announced transaction with Viatris is an exciting and significant step forward in building and expanding our emerging market footprint. With annualised sales of USD92 million (reported in December 2022) it will enable Latin America to become a key contributor to Regional Brands going forward. The product portfolio is expected to enhance current profitability ratios and importantly provides the region with increased critical mass in countries including Ecuador, Colombia, Peru, Chile, and Argentina supported by trusted key household brands including Viagra, Lipitor, Zyloft, Norvasc, Lyrica and Celebrex.

Ongoing challenges posed by regulated price reductions in countries such as Australia and below-inflation rate price increases in South Africa will be addressed by focusing on the growth of our OTC portfolio, launching new pipeline products, and strategically pursuing further value-accretive acquisitions, which will bulk up Aspen’s emerging market footprint.